Nordstrom Take-Private — Part I: Seattle Roots, Wall Street Blues

Four generations, poison pills, white knights and meme-stock lords

Prologue: a Christmas Miracle

While many of us were winding down our year, or furiously shopping on this last weekend before Christmas in 2024, the junior bankers at Morgan Stanley and Centerview Partners were hard at work preparing what they were hoping was their last deck for the board of directors of Nordstrom, the Seattle-based department store retailer.

If ‘deal fatigue’ needed a case study, Project Norse, as this mandate was coded, would be worthy of it. The board had been dealing with activism defense and reviewing strategic alternatives for the better part of two years. This board meeting, scheduled on Sunday December 22nd, was to be the sixteenth formal board update by financial advisors Morgan Stanley and Centerview since the beginning of the year.

The next morning, however, Nordstrom announced a definitive agreement with members of the Nordstrom Family and El Puerto de Liverpool, S.A.B. de C.V. (“Liverpool”), the Mexican department store group that already owned 9.9% of Nordstrom’s shares. The consortium was acquiring all of the outstanding shares they did not already own for $24.25 per share in a $6.3 billion deal worth ~5.5x 2024E EBITDA1. Following the closing of the transaction, Nordstrom would once again be a private company after more than fifty years in the public markets. The Nordstrom Family would own 50.1% and Liverpool 49.9%.

This was the family’s second go private attempt; the board rejected the first attempt by the Nordstroms to take the Company private dating back to 2018 when the board turned down an offer of $50 per share.

Once again, the juicy bits are in the SEC Filings as this $6 billion “going private” transaction falls under Rule 13e-3 of the Exchange Act, there are significantly higher disclosure requirements.

This deal has it all: fairness opinions, poison pills, meme-stock lords, valuation details, a dozen presentations from the investment banks and even disclosures from litigation. These board room documents provide unique insights into the challenges and decisions facing the Company.

Over two installments, I will take an in-depth look at this complex transaction, examining its history, challenges, and deal terms.

Flashback: a brief history of Nordstrom

From frontier shoes shop to national chain

The lore is that John W. Nordstrom arrived in New York in 1887 with five dollars and no English. A lucky stake in the Klondike gold rush yielded $13,000, seed money to open Wallin & Nordstrom, a 1,000-square-foot shoe with partner Carl. F. Wallin at Fourth & Pike in Seattle, Washington, in 1901. The formula was simple but radical for the era: offer every shoe size and width, maintain “open-stock” displays so customers handled merchandise freely, and treat returns as investments in goodwill.

John and Wallin eventually sold their shares to John’s sons Everett and Elmer by 1929. The company was dropped the Wallin name in 1930 to become just Nordstrom. John’s third son Lloyd joined the business in 1933. This would be the beginning of Nordstrom unique model of “management by committee.”

Over the next thirty years, Nordstrom expanded into women’s, men’s and children’s apparel and across state lines.

Management by committee.

By 1968, the company had reached about $50 million in sales when the third generation of Nordstroms stepped in, with Everett’s son Bruce, Elmer’s sons James and John, and Lloyd’s son-in-law Jack McMillan and family friend Bob Sender taking over from Everett, Elmer and Lloyd.

Under the leadership of what was an unorthodox leadership structure of four Co-Chairman, the following two and half decades would prove to be an astounding period of growth for the company. Between 1968 and 1995, the company grew sales at a remarkable 18% compounded annual growth rate, soaring from $50 million to an impressive $4 billion. This phenomenal streak transformed the retailer from a regional player to a national powerhouse, cementing its reputation as a leading department store chain.

In 1991, the four Nordstroms became Co-Chairmen. The fourth-generation Nordstroms were seen to be too young and inexperienced to lead the company’s rapid growth. They instead named four friends and managers as Co-Presidents, keeping with the tradition of leadership by committee.

In 1995 the four “Gen 3” Co-Chairmen retired to make the way for two of Co-Presidents, Ray Johnson and John Whitacre and, count them, six new Co-Presidents in Bill, Blake, Dan, Erik and Pete Nordstrom - all in their thirties at the time.

The four non-family Co-Presidents installed in 1991 had already been trimmed to two, and when Johnson retired in 1996 Whitacre was the last man standing. The board concluded that a lone CEO with deep store-ops experience would bring clearer accountability than the faltering committee model.

The more things change, they more they stay the same

In February 2000, Whitacre received board approval to eliminate the office of the Co-Presidency and to appoint presidents for each of Nordstrom's five business units. Appointed to those positions was only one Nordstrom, Blake, as President of Nordstrom Rack Group. The others were assigned various line jobs, including Dan as CEO of nascent Nordstrom.com2, Bill as EVP and East Coast General Manager, Erik as EVP and Northwest General Manager and Pete as director of full line store merchandising strategy.

general manager, while Pete is director of full line store merchandising strategy for

children’s apparel, cosmetics, junior apparel, lingerie, men’s apparel and women’s

active sportswear.

Only seven months later in September 2000, Whitacre was ousted as CEO as his attempt to rejuvenate assortment and attract younger customers alienate its customer core base without attracting enough new ones.

With hip-hop music and flashing lights, Nordstrom has been trying to get shoppers to trade tweed blazers for leather miniskirts. Ads have been urging customers, "Reinvent Yourself."

Many Nordstrom loyalists were put off by the stores' more visible -- and audible -- changes. Older customers didn't necessarily take well to throbbing strains of hip-hop or all that black leather draped around.

Bruce Nordstrom came out of retirement to assume the role of Chairman with his son Blake as sole President. The family was back in charge.

With Bruce and Blake at the helm, the family was quietly betting that the old Nordstrom formula - merchandising instinct backed by obsessive service - could still outperform the . Re-centralizing buying steadied the floor: from $5.7bn in sales in 2000, comps turned positive in 2002, sales accelerated through the mid-decade, weathered the GFC before roaring back to hit $14.4bn in sales in 2015. The brothers rolled out Racks at a ferocious clip and also invested heavily into their e-commerce platform. The stock hit an all time of $82 in March of 2015 and brothers Pete and Erik joined Blake as Co-Presidents that same year.

By 2017, however, the mood had shifted as new channels were eating into department stores’ share of the US apparel market: Amazon was plowing its way through retail, brands were leaning into their own direct-to-consumer channels and fast-fashion was hot. Growth was stalling and the combination of lower store footfall and the new retail landscape (with free shipping, e-commerce capabilities, and price-matching offers) was proving to be margin dilutive.

The 2017 take-private overture

The filing that woke everyone up

On June 7th, 2017, barely three weeks after a disappointing earnings report that sent the share price down near 18%, members of the Nordstrom family representing 31% of the outstanding shares of the company disclosed through a Form 13-D regulatory filing that, “in light of the changing dynamics in the retail environment, [the Nordstrom Family] determined to form a group (the ‘Group’) to explore the possibility of pursuing a ‘going private transaction’ involving the acquisition by the Group of 100% of the outstanding shares” of the company.

In that same filing, the Nordstroms also made it clear that, should the board want to expand the process to other potential bidders, they were neither interested nor supportive of a sale of the company to a third party:

As heirs to the [Company’s] co-founder, and following four generations of family leadership of the business that bears their name, the [Nordstrom Family], in their capacities as shareholders of the [Company], have no interest in a sale of their shares of Common Stock of the [Company] to a third party, or voting for an alternative transaction.

- Form 13-D, June 7 2017

No offer was made and the filing specifically noted that “At this time, the [Nordstrom Family] have not secured commitments for any such debt or equity financing and there can be no assurance that [they] will be able to obtain the funds necessary to consummate one or more of the transactions described.”

Nevertheless, the family engaged Moelis while the board formed a special committee hired and Centerview as its financial advisor. The stock promptly popped 17%.

Why make such an announcement without a definite proposal?

Due to one of the peculiarities of Washington State law - the RCW 23B.19 “moratorium” statute - the Nordstrom family had little choice but to lay their cards on the table. Owning well over the 10 % threshold that triggers the statute, the family knew any quiet, behind-the-scenes buy-out effort would be blocked for five years unless an independent committee of the board first sanctioned their buyer group and the deal later passed a “majority-of-the-minority” vote. By publicly declaring their intent, they compelled the board to form that committee, satisfied securities-law disclosure, essentially invited lenders and potential equity partners into a fully authorized process, and, while doing so signaled to third parties that their ultimate consent to a transaction was non-negotiable.

Dialing for LBO dollars

The next several months would have the Nordstrom and their advisor Moelis canvassing equity and debt financing providers. At the time, a transaction at $50 per share implied an equity and enterprise values of about $8.4 billion and $10.0 billion, respectively. Private equity firm Leonard Green showed interest to partner on the deal but financing the transaction was the challenge. Retail LBOs were out of favor in the leveraged capital markets, especially with the bankruptcy of KKR owned Toys R Us in September 2017 and the challenges of debt ladened fellow luxury department store company Neiman Marcus3.

By March 2018, however, it appeared that Nordstroms and Leonard Green had secured the financing for a deal at $50 per share. With Nordstrom’s share price trading around $52 at the time and hopeful memories of the $82 all-time-high in 2015, the board rejected the offer. After the family declined to raise its bid, the board terminated all discussions, noting in the press release that the parties “could not reach agreement on an acceptable price.” Nearly a year’s work had just gone down the drain.

The next few years would continue to be challenging for the company and the family. In January 2019, Co-President Blake Nordstrom passed away unexpectedly. This was quickly followed by the shock of the pandemic the next year, with sales falling 30% to $11 billion. Then, in late 2021, Bloomberg revealed that Nordstrom had hired AlixPartners to study a spin-off of the off-price Rack division, the same break-up logic activists were pressing at Macy’s and Kohl’s at the time. While the company framed the review as internal and no activist had publicly raised its hear, bankers claimed it was in direct response to prospective shareholder pressure for value-unlock options.

Enter Liverpool, the Mexican White Knight?

We may never know the full story, but the official one is that Liverpool CEO Graciano Guichard González met Blake, Erik and Pete Nordstrom at an industry conference in May 2017 where they swapped merchandising war stories. The families shared legacies as a family-founded and family run businesses together with a gospel of attentive service and credit-card analytics. Liverpool’s cash rich balance sheet was also the envy of battered U.S. peers. The two sides remained in contact and met at other conferences in 2018 and 2019.

In January 2022, according to the proxy statement, Liverpool expressed their interest to Erik and Peter in using excess cash on their balance sheet to make a passive minority equity investment with no intention of exerting any control or influence over Nordstrom.

In late August 2022 - with the Nordstrom share price dipping under $20 - Liverpool quietly began buying Nordstrom stock on the open market, disclosing a 9.9% passive stake on 15 September 2022. Alarmed at a potential creeping takeover, Nordstrom’s board installed a 10 percent shareholders rights plan, a soft poison pill that nevertheless signaled welcome if Liverpool played by the rules.

Far from repelling suitors, the move cemented a friendship. Liverpool executives toured with Nordstrom merchants, brainstorming cross-border private-label sourcing.

The end result was also that now more than 40% of Nordstrom’s shares were in the safe hands.

Reality Check

While Nordstrom was reasonably safe from a hostile takeover or shareholder activists, it did not stop Ryan Cohen, the meme stock king and billionaire co-founder of pet retailer Chewy, from giving it a shot. In February 2023, the WSJ reported that Cohen was amassing a sizable stake in Nordstrom and was agitating for board changes and cost cuts amid sluggish sales. Even though Cohen never filed a proxy slate and the campaign fizzled by mid-2023, it was a catalyst for the board to take action.

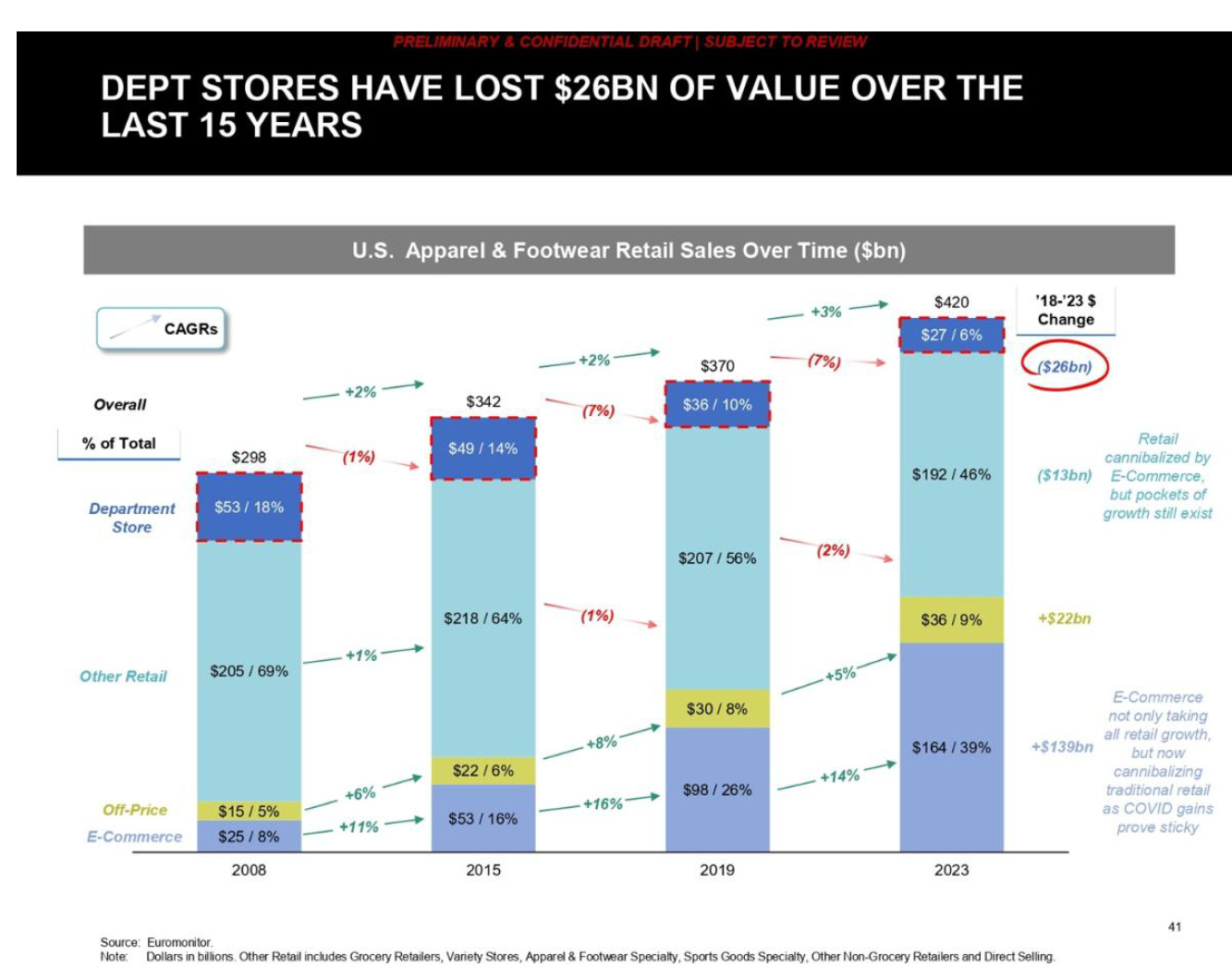

At a meeting in June 2023, the board discussed initiating a review of strategic alternatives that might be available to enhance shareholder value.

During that meeting invited guest Morgan Stanley likely showed some version of the two slides below. The headline was bleak: department stores had lost $26 billion of sales - half their business - in the last fifteen years.

What to do now?

To be continued…

In Part II we will see where Nordstrom’s review of strategic alternatives takes them, the challenge of finding value creation solutions, and how the Nordstrom Family and Liverpool eventually secured the approval of the board. We will also glean precious insights from the presentations of the advisors on the transaction. Stay tuned.

In the mean time, read all about the largest packaged foods deal in 10 years.

Extract from board update dated 19 December 2024:

Throwback: Nordstrom website from 2000. Couldn’t resist including.

Neiman Marcus would eventually file for bankruptcy protection in 2020.